DAN CAIRD

Mortgage Agent, Level 2

Sound mortgage advice and fantastic mortgage rates, simply guaranteed. Let me guide you through the mortgage process.

Mortgage financing can be frustrating. It doesn’t have to be when you follow my simple 3-step plan.

Get started right away

The best place to start is to connect with me directly. The mortgage process is personal. My commitment is to listen to all your needs, assess your financial situation, and provide you with a clear plan forward.

Get a clear plan

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming. Let me cut through the noise, I'll outline the best mortgage products available, with your needs in mind.

Let me handle the details

When it comes time to arrange your mortgage, I have the experience to bring it together. I'll make sure you know exactly where you stand at all times. No surprises. I've got you covered.

Meet Our Team

Get to know the people behind our work

Dan Caird

LEAD MORTGAGE SPECIALIST

With over a decade of experience in the mortgage industry, Dan works closely with clients to help make the mortgage process feel simple, clear, and as stress free as possible. Whether you’re buying your first home, refinancing, renewing, or investing in property, he takes the time to understand your goals and find the best fit for your situation. Known for being approachable, responsive, and easy to work with, Dan is always happy to answer questions and guide clients through every step of the process.

Kareen Afar

MORTGAGE SPECIALIST | DIRECTOR OF WOW

Kareen Afar is a dedicated mortgage professional and the Director of WOW on the Dan Caird team. She leads the post funding client experience, ensuring clients continue to feel supported, valued, and well taken care of long after their mortgage is in place.

Kareen connects with clients following funding and provides ongoing proactive check ins, guidance, and support to help them make the most of their mortgage over time. Known for her strong communication, attention to detail, and client focused approach, she plays a key role in building long term relationships and delivering the level of service clients expect from the Dan Caird team.

Sarah Ornopia

CLIENT RELATIONS COORDINATOR

When you work with us, Sarah will often be the one keeping in touch throughout the mortgage process, whether that’s collecting documents, providing updates after an approval, or helping coordinate any remaining lender conditions.

I personally handle the mortgage strategy, including reviewing the file, determining which lender is the best fit for your situation, and submitting and negotiating the mortgage application itself. Sarah helps ensure everything stays organized, on track, and as stress free as possible throughout the process.

Known for being friendly, responsive, and easy to work with, Sarah is always happy to answer questions and help clients feel informed and supported every step of the way.

I'm happy to provide you with a wide range of Commercial Mortgage financing options.

Commercial financing solutions tailored to your needs, including multi family residential, construction financing, owner occupied properties, investment real estate, and business loans.

Working with clients across the GTA and Durham Region, I have access to a wide range of mortgage products and some of the most competitive rates available in Canada. My goal is to help make the financing process clear, smooth, and as stress-free as possible.

If you ever have questions, I'm always just a phone call, text message or email away

MEMBER OF THE CANADIAN MORTGAGE BROKERS ASSOCIATION.

CMBA provides Canada’s provincial mortgage broker associations with a forum to work cooperatively, better share resources, programs, and information and coordinate engagement of provincial association members to identify trends and develop solutions to common industry and regulatory issues.

I have developed excellent relationships with lenders across

the country, when you work with me, you have choices.

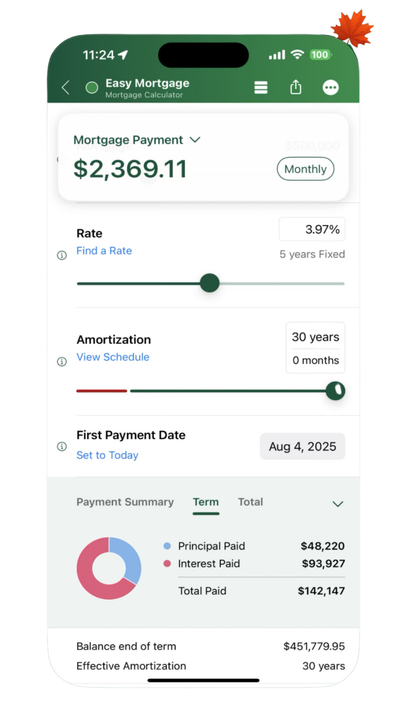

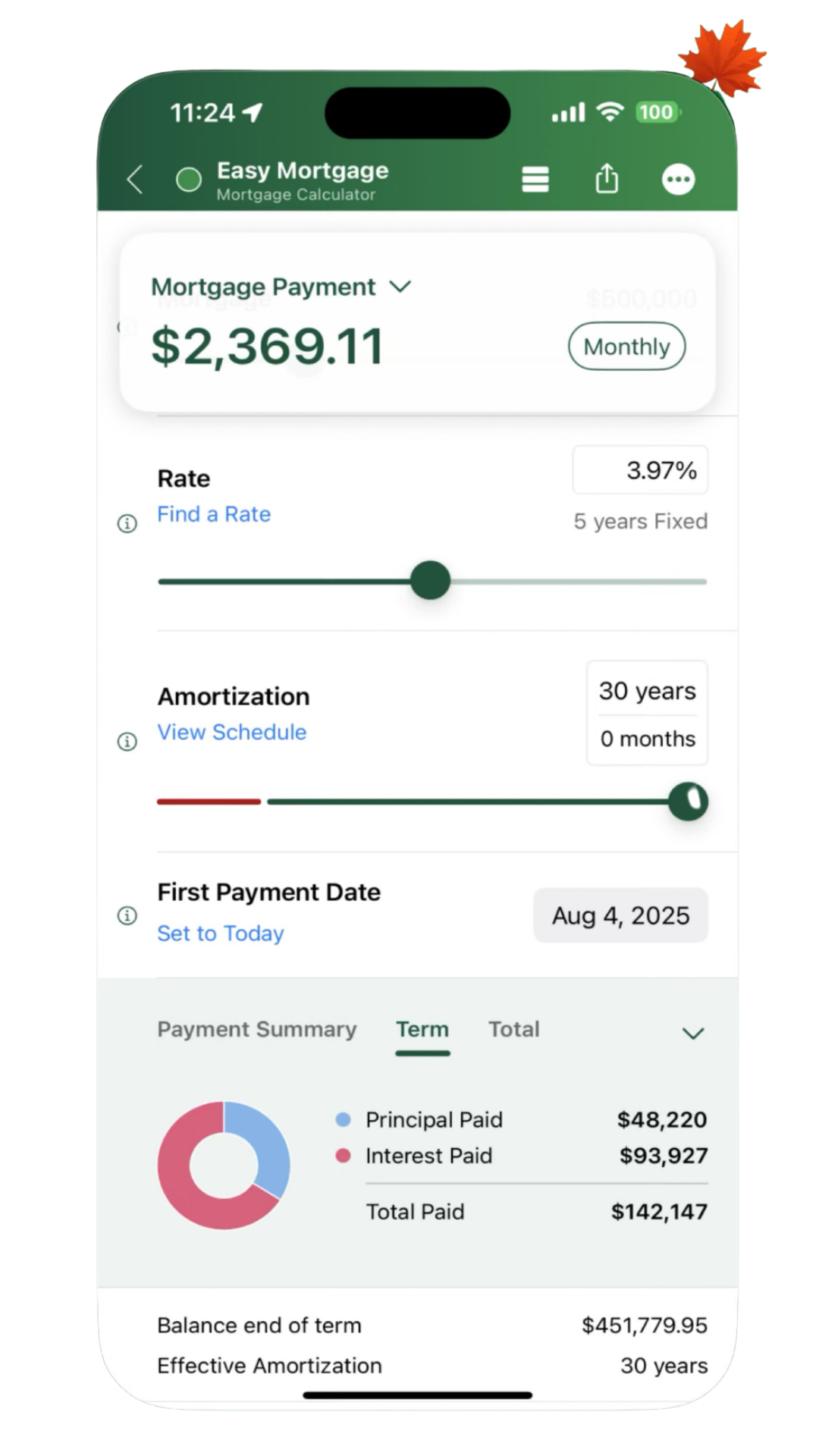

Mortgage Articles